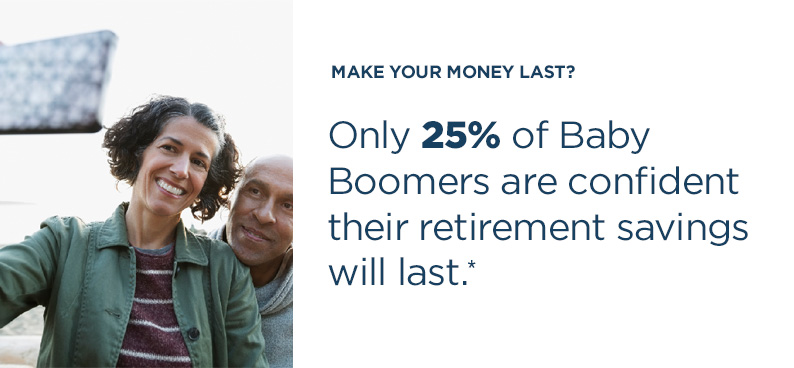

For decades, you’ve been working hard and saving for your retirement.

But when the big day comes and

you actually do retire, will you be

ready to use what you’ve saved to:

*https://www.irionline.org/resources/resources-detail-view/boomer-expectations-for-retirement-2018

Paying for the basics. Having money that won’t run out. Leaving your family with income. Let’s see how to make your money work smarter to help you reach your retirement goals. We’re in the business helping people like you become income ready for your retirement. Learn how Global Atlantic can help you realize your retirement goals.

Get income insight

See what everyday people think about retirement income.

Ready to retire? Sure! Have enough money to last throughout retirement – not so sure. Watch this video to see what people think about protecting part of their money for retirement.

Help fund your "paycheck"

See how to add lift to your retirement income strategy.

Before you launch your retirement journey, play this short video to consider the income sources you'll use for your “paycheck."

|

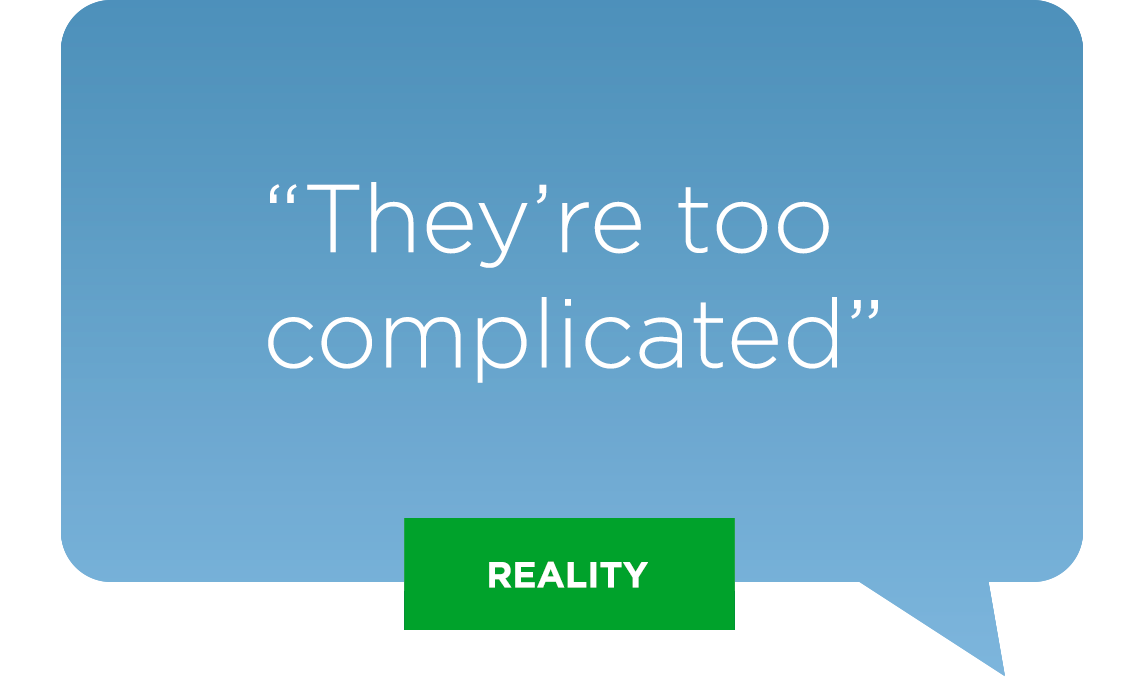

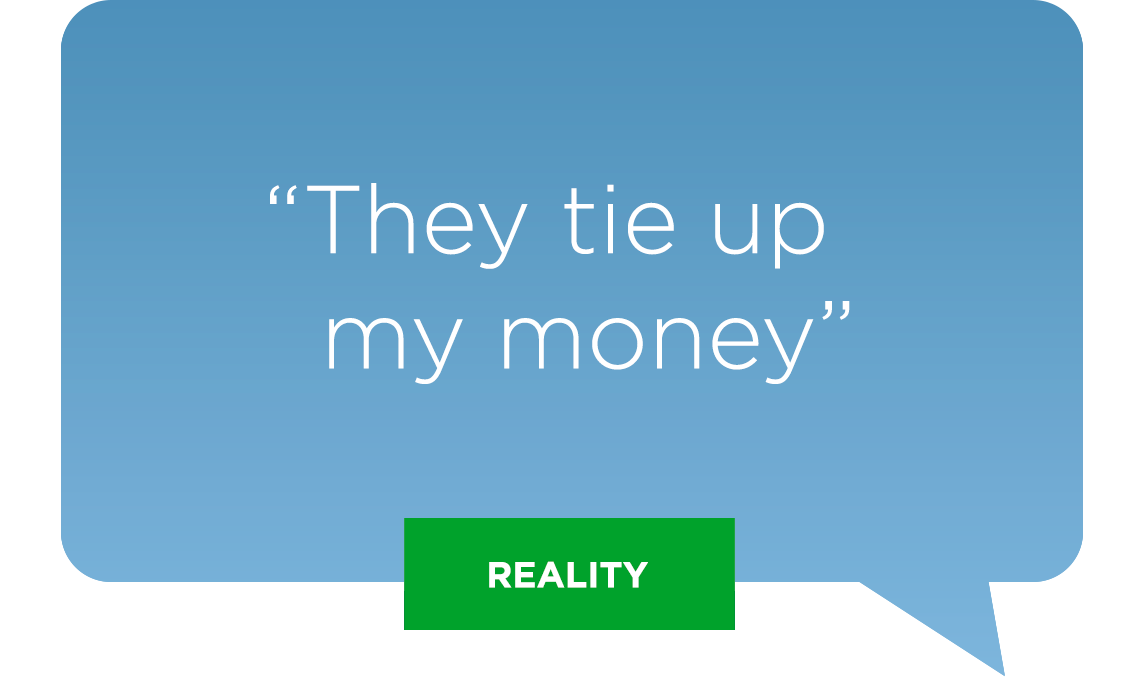

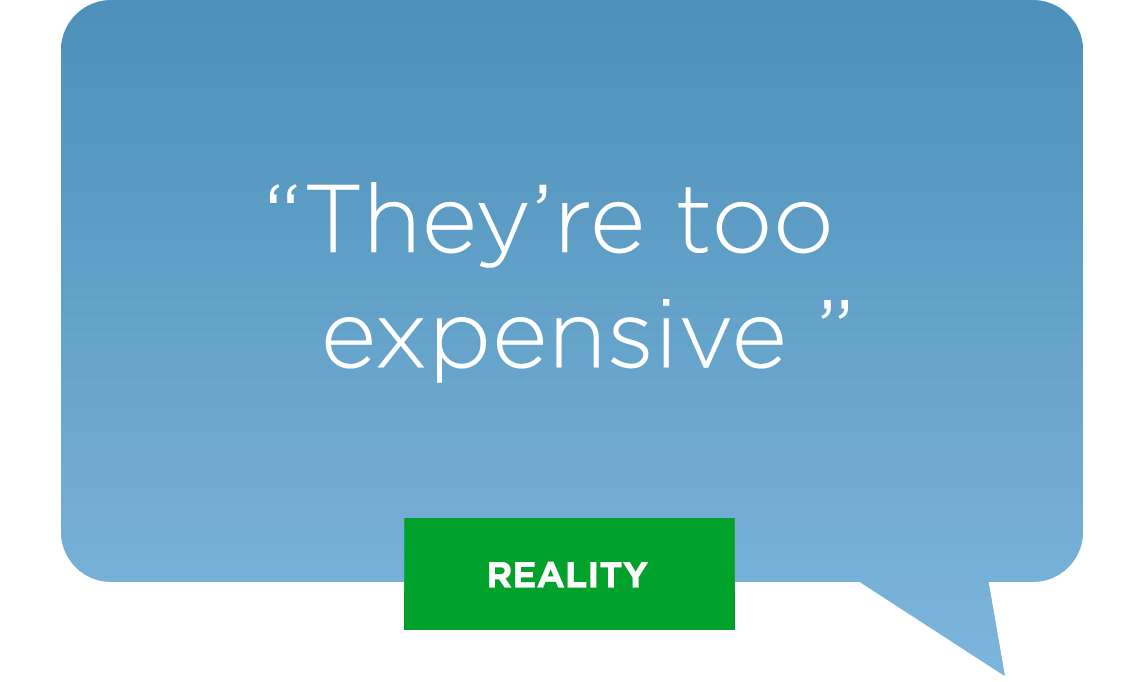

Perception vs. Reality

The myths and facts of income annuities.

A fixed index annuity may be the income source you need, but you may have strong opinions about the "A" word: an annuity. Discover some of the common misconceptions and then click the “reality” button to learn the real story about annuities.

Fixed Index Annuity reality:

ONE: FIAs offer growth potential with no market-based losses.

TWO: FIAs may also offer protected lifetime income.

With an FIA, you may potentially grow your money through interest that’s credited to your contract. FIA interest crediting may be calculated in one of two ways:

- 1. AN INDEX-BASED STRATEGY credits interest each crediting strategy term based, in part, on the performance of one or more market indices, such as the S&P 500.1, 2

- 2. A FIXED-BASED STRATEGY credits a specific, consistent percent of interest each crediting strategy term to the FIA.

An FIA may also offer you the option of building a “retirement paycheck” for life that won’t go down due to down market performance and can’t be outlived.

An objective indicator of changes across a market – or a market sector – based on the performance of representative securities.

WHAT IS THE S&P 500?

An unmanaged index that measures broad-based changes in stock market conditions based on the performance of 500 widely held U.S. common stocks.

1 Indices are typically unmanaged and not available for direct investment.

2 “Standard & Poor’s®”, “S&P®”, “Standard & Poor’s 500™” and “S&P 500®” are trademarks of Standard & Poor’s Financial Services LLC and have been licensed for use by Forethought Life Insurance Company. Fixed index annuities are not endorsed, sold or promoted by Standard & Poor’s and Standard & Poor’s does not make any representation regarding the advisability of purchasing a fixed index annuity contract.

Fixed index annuity reality:

FIAs typically allow you to withdraw a percentage (10% is common) of your annuity “contract value” annually after the first year.

Fixed index annuity reality:

Fixed index annuity reality:

• Your fixed index annuity contract value won’t go down due to negative market performances1

• Your opportunity for guaranteed lifetime income could be more money than what you paid for your fixed index annuity.

• Any remaining contract value gets passed to your beneficiaries as a standard death benefit.

Guarantees are based on the claims-paying ability of issuer and assume compliance with the product’s benefit rules, as applicable.