How to help your clients through divorce, widowhood, and caregiving

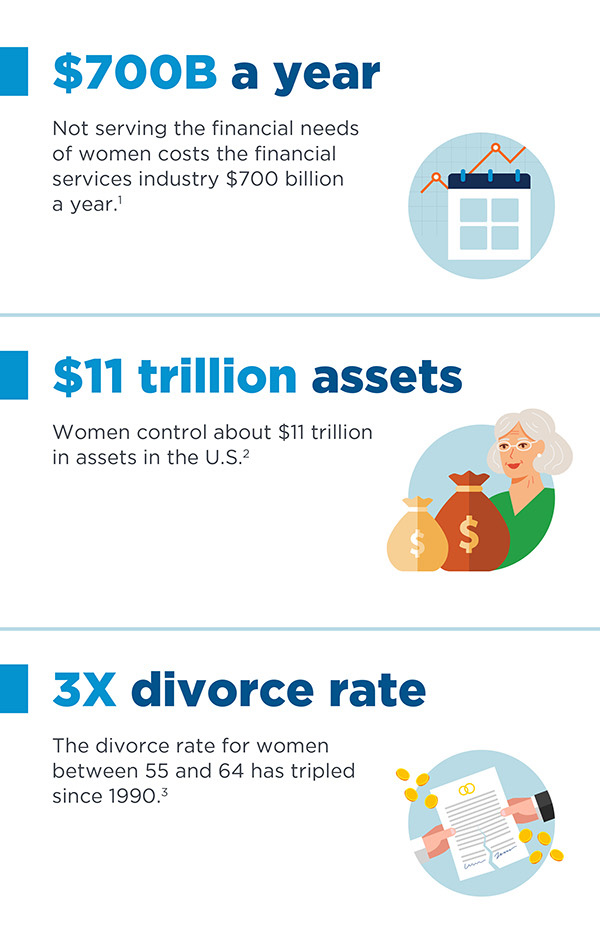

A key group of clients for financial professionals to target is women, a segment of the population that has long been neglected by the financial services industry. Making that point, Oliver Wyman, a leading management consulting firm, noted in a 2020 report that the industry has left nearly $700 billion a year on the table by failing to address the unique financial challenges women face.1

The study explains that “in a $4 trillion revenue industry that is currently growing below GDP growth rates, this is arguably the largest single growth opportunity out there.” In fact, the consulting firm McKinsey & Company estimates that women control almost $11 trillion in assets2 in the U.S. today, a number that will only increase as male baby boomers die and transfer their assets to their female spouses, who tend to outlive them by more than five years.6

Now, more than ever, there is a tremendous need for financial professionals who understand the challenges women face and who know how to work with them.

Among those challenges, few are more pressing than three circumstances in which women over the age of 50 are increasingly finding themselves: divorce, widowhood, and caregiving. Each of these circumstances also present challenges—and opportunities—for financial professionals (see sidebar for specific actions to take). As Ann Hughes, founder and president of The Female Affect, a group established to help financial professionals tap into women’s needs for financial services, puts it, “We are seeing a shift in women saying, ‘I need advice’ to ‘I want advice.’”

“The industry has left nearly $700 billion a year on the table by failing to address the unique financial challenges women face.1”

Shades of gray divorce

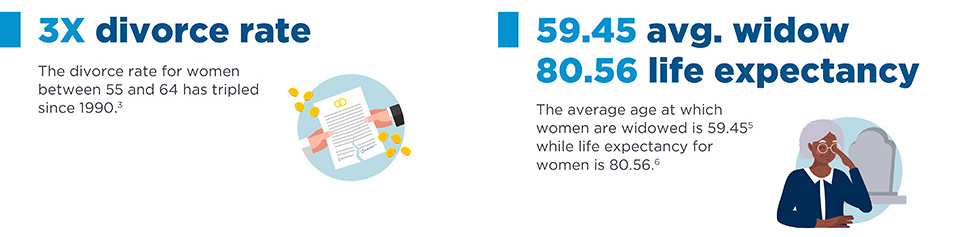

Divorce among older couples—known as “gray divorce”—is growing faster than the divorce rates among any other group. For women between 55 and 64, the divorce rate has tripled since 1990; it’s increased six-fold for women over 65, according to a study by the National Center for Family & Marriage Research at Bowling Green University3.

The unfortunate reality is that, for many women in these age groups, the “marital deal” struck early in their marriages left the husband in charge of both finances and dealing with the family’s financial planner. Left alone, and often facing a decreased standard of living, these divorced women need information, support, and guidance when it comes to navigating their financial futures.

The reason for the raft of gray divorces among baby boomers varies from couple to couple. When Elliot Wiener, a divorce attorney with Phillips Nizer in New York City, asked a divorcing wife why she was ending her marriage, her reply was simply, “I just don’t love him anymore, and I’m only here once,” echoing the mantras baby boomers often recited in their more formative years: “life is short” and “happiness matters.” But faced with divorce, Wiener notes, many of his older female clients often lack even basic financial literacy. “They don’t know anything about their own finances because ‘he’ handled the money,” Wiener explains.

And this issue is exacerbated by circumstance. According to Susan Brown, a sociology professor at Bowling Green State University, women divorcing after age 50 generally find that their financial worth plunges by 45%, more than twice the loss experienced by men over 50 and younger women facing divorce.4 As Brown noted, “Older adults are unlikely to recoup financial losses associated with divorce, and this is particularly true for women who were out of the labor force for decades.”

A financial professional who can help navigate unfamiliar terrain and set lifestyle expectations following a decrease in assets, while understanding the needs of female clients during an emotionally fraught period, can make a significant difference in their long-term financial wellbeing.

Life after widowhood

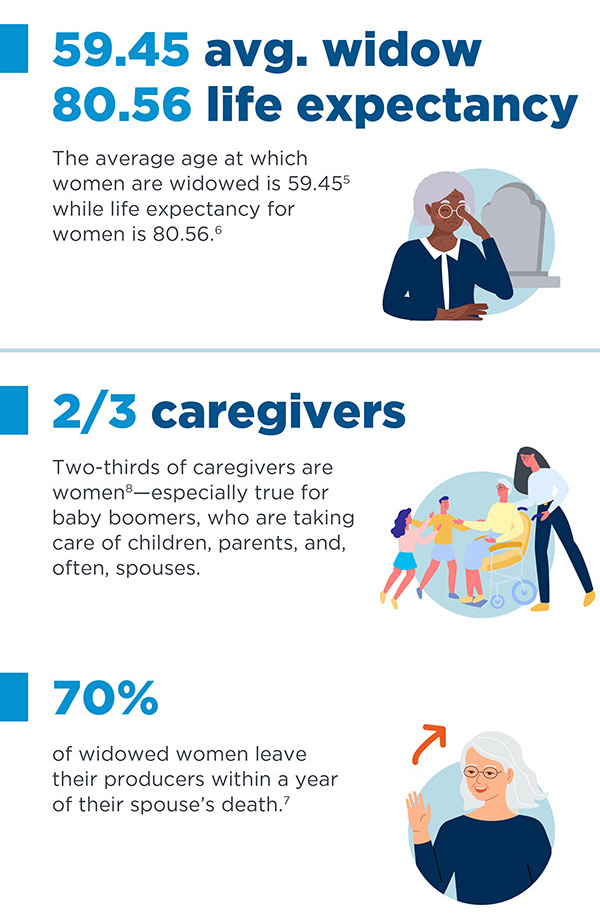

The average age at which women become widows in the United States is 59.4.5 Life expectancy for women in the U.S. is 80.5.6 This means many widows have decades left in which to manage their finances without the financial support of a spouse. And as is the case with older women facing divorce, a large percentage of widowed baby boomers have not been actively involved in financial planning.

“In many baby boomer couples, men take on the long-term planning while women tend to be responsible for the short-term day-to-day budgeting,” says Jeannie Underwood-Kotner, SVP, head of Global Atlantic Consulting at Global Atlantic Financial Group. It’s critical, she notes, that the financial professional build a relationship with the woman in the couple “way before widowhood.” In the event of a death, she explains, it’s likely that friends and relatives will flood the new widow with referrals and advice.

Overwhelmed by these suggestions, shattered by loss, and lacking strong ties to a financial professional, some 70% of widows leave the financial professionals who had represented the couple within a year of a spouse’s death.7 If the relationship has not already been built, Underwood-Kotner stresses, it may well be too late to retain them as a client.

However, financial professionals who had worked to develop strong relationships with their female clients prior to widowhood—and those who are quickly able to build these relationships by projecting genuine empathy and an understanding of the client’s fears and goals, are more likely to be successful at retention. “It’s the little things that can have the biggest impact, especially with women,” says Underwood-Kotner. “You have to have awareness for yourself and the ones you want to work with.”

Balanced caregiving

Baby boomers have often been called “the sandwich generation,” caught between caring for children and aging parents. And as these boomers age, they’re increasingly providing care for ailing spouses as well. Two-thirds of the caregivers are women,8 and the time they spend prioritizing family over careers cuts deeply into both their earning potential and their financial future. “Caregiving is bringing down our women baby boomers,” says Underwood-Kotner. Hughes agrees. “By nature, women are nurturers to the detriment of their own financial wellbeing,” she says. In fact, a study by the MetLife Mature Market Institute estimated that women forfeit an average of nearly $143,000 in income to tend to their caregiving responsibilities.9 Add to that the money they spend on out-of-pocket expenses, such as supplementing an older relative’s budget or paying for a child’s education, and it’s not surprising that the risk to their financial future is so great. Hughes notes, for example, that women over 65 are far more likely than younger women to fall into poverty.10 “Professionals can help put up guard rails to operate in and can give perspective on how much she can provide to others in her caregiving role without sacrificing her own financial wellbeing,” she says.

Feeling valued

Whether a woman is facing gray divorce, widowhood, or caregiving, the financial challenges can be daunting, especially for older women who have not participated in long-term financial planning decisions. Although men have traditionally dominated those conversations, Hughes believes that institutions are now making a stronger effort to reach women directly, especially given that women now control more wealth and have expressed more interest in becoming financially savvy. “There is a concerted effort from the largest financial services companies that are devoting money and resources to training and developing their financial professionals so that they can relate to women on their terms,” Hughes says.

This shift in thinking has been a long time coming, adds Underwood-Kotner. Financial professionals “know it, but they just can’t cross over.” She points to the growing trend of producers working in teams to better serve female clients. Whether an a financial professional works within a team or acts as an individual, Underwood-Kotner says the key to success comes down to basics. “It’s connection and feeling valued,” she says. “Women want to work with someone who will help them with who they want to be and with what they want to do with their life.”

How to Work with Your Female Clients in Their Hour of Need

- Show how much you value them.

- While meeting with couples, make eye contact with her to make her feel that her input is important, and welcome her participation.

- Be a good listener, take notes, and encourage her to ask questions to enhance her understanding of financial matters.

- Ask her how you can best communicate with her—and how often—to show that you respect her time and attention.

- Create a professional office environment that instills confidence and reflects your personality so she can better connect with you on a personal level. Maximize the opportunity to expand on her questions about, for example, your office decor to get to know her beyond just her financial picture.

When divorce or widowhood strikes

- Resist the urge to go into autopilot. Though you may have dealt with many divorces and spousal deaths, this is likely her first. Allow her to express her emotions—and listen intently.

- Ask open-ended questions to open the lines of communication regarding her unique circumstances, fears, and goals. By understanding these matters, you can better assess her level of financial literacy and collaborate with her on the best course of action toward the life she wants to live.

- Recognize that there are many decisions to be made and break them down into chunks and timelines so she doesn’t feel she has to do everything at once. Be methodical and act as her voice of reason during this traumatic and emotional time.

- Become a resource to her and offer ongoing support to show that you see her as a human being and not just as a collection of financial assets. Develop a network of professionals to refer her to that address her life needs outside of her finances.

When caregiving becomes a financial burden

- Educate her on the larger financial picture. Caregiving is a choice driven by emotions, and her short-term decisions will have long-term effects.

- Avoid the “white horse” syndrome, where you tell her there is no need to worry. Though she wants reassurance, she also wants to hear your suggestions for how to better manage her money. She does not want to be told what to do and would prefer to be given the information to help determine her own future.

- Try to understand her unique circumstances to help her establish a plan that will allow her to continue being a caregiver without putting herself in financial jeopardy. By offering an outside perspective on her situation, you can help establish boundaries for spending and help her apply logic to her emotional decisions.

Share

Related resources

Your Thriving

Practice

A destination to empower financial professionals to build, manage, and grow their practice

Get started with Global Atlantic

Take the next step with a company that can help elevate your business.

Need help?

Find all the contact information to submit and service your business.